eLearning Log in

Login here using your username and password

How do I manage project costs?

Introduction

Performance against forecasted budget is an essential reporting requirement. The main costs for a project will come under two headings: resources and assets. The control activities around costs are very much linked to the controls around time as the time required from the resources represents significant costs.

The costs of assets should be known or established as part of the procurement process, either through formal tendering or gaining quotations. Variations in cost are likely to be linked to changes in requirements or specification by the operational areas or the suppliers offering additional facilities that increase the costs. Any changes to cost must be raised as a change request and managed through change control.

If the project business case is justified on benefits, careful monitoring of the changes from the baseline cost estimate against the planned benefits is essential. There may be a tipping point where there the benefits are no longer achievable and the project should be stopped, and the earlier this is spotted the better.

Earlier in the project estimates will have been created for the different types of resources. Although not all of these are tracked as costs, because they are internal, availability, performance and consumption of these resources will be a critical success factor for the project, for the following reasons:

This extract has been reproduced with permission from A Practical Guide to Project Planning, TSO 2016. If you’d like to read more you can purchase the copy of the book here.

- Using external resources at a faster rate than was anticipated will cause problems with later tasks

- Using operational resources earlier than planned will mean they may not be available later

- Over-utilization of operational resources that have not been accounted for may alienate the stakeholders and lead to loss of cooperation

- Being under budget against the plan could mean that the project is either ahead of or behind schedule. This could be because the expenditure is being postponed due to procurement delays.

It is important to assess, as early as possible, whether resources are being over-utilized or are not available when required. This information should be used to re-assess the plan, and, if necessary, to recast the stage plan at least. Some reasons for resource estimates being wrong include:

- Estimates were based on wrong comparisons or experiences

- Individual or group competencies are inadequate

- There is over-reliance on one or two key individuals

- Underestimation of the complexity of the tasks that contribute to the asset costs

- Stakeholders failing to deliver their commitments and delaying procurement

- Resource conflicts with other projects operating in that area, and operations overcommitted

- Events in the supply chain or operations that are drawing on resources anticipated being available to projects

- Assets not actually available for procurement

- Assets do not meet specification.

Technique

As with time management, the cost analysis should be based on the expected costs and the tolerance that may have been allocated to the project. The technique for managing costs is also essentially the same as for managing time, namely:

- l Analysing the budget against the baseline and determining which areas may need corrective action

- l Deciding what specific corrective actions should be taken

- l Revising the plan to incorporate the chosen corrective actions

- l Recalculating the budget to evaluate the effects of the planned corrective actions.

Delays should be assessed by considering their impacts on the following:

- l Capital budget

- l Revenue budget

- l Expenditure profile

- l Projected availability of funds

- l Benefits plan.

Example

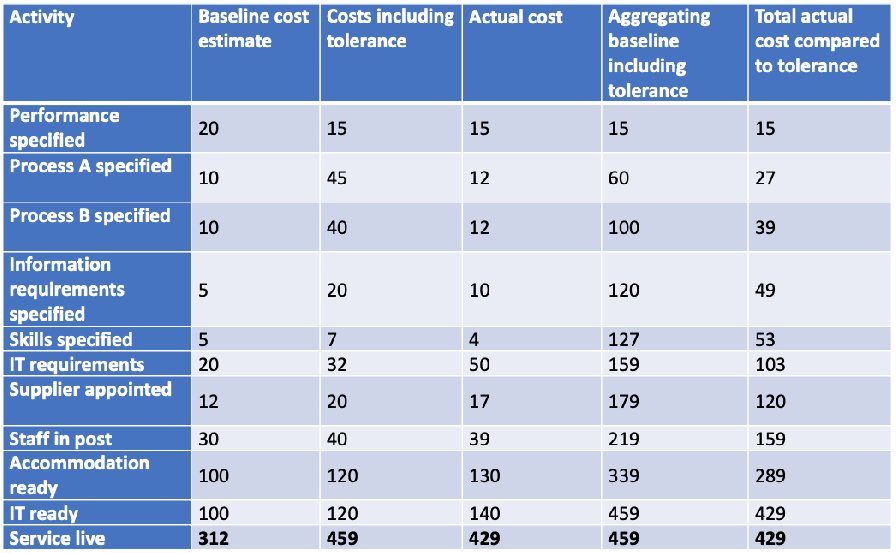

Table 5.8 shows variation between planned and actual costs using the same example as in the previous section.

Variation report for planned versus actual cost

In the example in Table 5.8, the project comes in over budget because of a significant later overspend on IT and accommodation but is still within overall tolerance.